August 7, 2020 Reading Time: 19 minutes

Reading Time: 19 min read

Image Credits: Dhammika Heenpella/flickr

*Ganeshan Wignaraja

The past decade has seen Asian economies experiencing a boom in mega infrastructure initiatives (MIIs) partly linked to the region’s global economic rise and great power rivalries. China’s Belt and Road (BRI) initiative—a massive trans-continental programme which seeks to improve regional connectivity and cooperation—is grabbing international headlines with a plethora of eye-catching projects (See Hillman, 2018; Prasad, 2018; Wignaraja, Panditaratne, Kannangara, and Hundlani, 2020). However, the BRI has come under greater scrutiny recently, with growing worries about “white elephant projects”, “Chinese debt traps”, and “Asian countries being engulfed in a string of Chinese pearls” (Macaes, 2019; Saara, 2019). The US has also put forward a Free and Open Indo-Pacific (FOIP) initiative with an infrastructure component. Japan, the EU, and ASEAN are following suit. The advent of the COVID-19 global pandemic in 2020 has intensified great power rivalries in Asia and prompted talk of China’s coronavirus diplomacy and a second cold war (Poling, 2020). The economic impact of multiple MIIs on Asian economies is not well understood in policy circles due to their recent emergence and the lack of project-level evaluation studies.

How can Asia recipient economies, particularly the region’s smaller and more vulnerable economies, reap the benefits of MIIs while minimizing their costs, is an important policy question to aid economic recovery from the COVID-19 pandemic. This LKI Policy Brief examines this question through the lens of the literature on regional economic integration and cost-benefit analysis.1 Section II discusses the link between infrastructure investment and economic development in Asia. Section III maps the growth and features of MIIs. Section IV assesses emerging “noodle bowl” risks from MIIs while Section V looks key ingredients of national strategies in recipients to mitigate such risks.

One of the lessons from Asia’s economic miracle story was the impressive savings and investment rates, deliberately promoted by governments (Stiglitz, 2001). A major aspect was the role of national infrastructure investments (transportation, power, water, and telecommunications systems) in facilitating trade and growth. Famous examples of trade-related infrastructure projects are available from newly industrialising economies (NIEs) in East Asia. South Korea invested USD 10 billion to build the Busan Port, which today handles about three-quarters of the country’s container traffic. Singapore invested around USD 6 billion to construct Changi Airport, which has become one of Southeast Asia’s busiest transport hubs, annually moving over 60 million people and over 2 million tonnes of air freight. These investments have helped both economies to experience rapid structural transformation and growth over several decades. Per capita incomes have risen rapidly and enabled Korea and Singapore to become high-income economies.

More recently, Asia has invested in regional infrastructure to link neighbouring countries and more distant countries for trade-led development (Arnold, 2009). Most of the trade within Asia follows an ocean route with seaports providing connectivity to Southern coastal areas where much of the population and production is located. There is also increasing effort being made to create Northern land routes to access areas beyond the coast such as landlocked countries or inland areas of China and India.

The notion of investing in regional infrastructure has roots in the economic literature on geography and trade pioneered by Krugman (1991) and others. It highlights the notion that geographical considerations influence the volume of trade between countries. Gravity models confirm that distance matters for trade, with each doubling of distance between countries halving the volume of trade (Venables, 2019). Studies also indicate significant trade frictions such as transport costs and cumbersome border management systems. Such costs between neighbours can be reduced by building roads, railways, power transmission lines, and other hardware for regional connectivity. The Kunming-Singapore railway, often labelled the Pan-Asian Railway Network, which links China, Singapore, and other Southeast Asian countries, is an important example. This builds upon a fragmented railway network that originated in British and French colonial times. Another is the Central Asia Road Links Programme of the World Bank, which aims to improve road connectivity between Tajikistan, Kyrgyz Republic, and Uzbekistan. Software projects in the form of streamlined customs procedures and e-boarder management systems also complement hardware for regional connectivity.

There is little doubt that such cross-border projects have contributed to Asia’s rapid economic development, by stimulating flows of goods, services, investment, and people across the borders of neighbouring countries. By improving connectivity, they have also fostered regional peace and cooperation among the region’s small and large countries alike. Safeguards and public policies have been pursued to reduce negative effects from such projects, including displaced people, environmental degradation, and crime.

Model-based studies have shown that significant welfare gains can be achieved by investing in physical connectivity and associated software to link parts of Asia. As part of the work related to the Comprehensive Asia Development Plan (ERIA 2010) prepared by the Economic Research Institute for ASEAN and East Asia (ERIA) for the East Asian Summit, Kumagai et al. (2013) used the IDE/ERIA geographical simulation model, a detailed regional model, to estimate impacts on the cumulative increase of GDP of countries in the two regions from 2010–30 relative to the base case for a number of connectivity projects, including the Mekong-India Economic Corridor (MIEC), the Dawei and Kyaukphyu deep seaports in Myanmar, and the India-Myanmar-Thailand Trilateral Highway. For the MIEC alone, they found cumulative impacts of over 5% of GDP for Cambodia, Myanmar, Thailand, and Vietnam, and over 2.5% for India.

Wignaraja, Morgan, Plummer, and Zhai (2015) examined the welfare gains from connecting South and Southeast Asian economies. The study uses an advanced CGE model featuring recent innovations in heterogeneous firms trade theory into the CGE framework. One of its most striking findings is the vast size of potential economic gains from infrastructure-led integration, amounting to at least USD 568 billion. This is a conservative estimate under a comprehensive integration scenario. The study finds that more populous South Asia would see a larger gain of USD 375 billion (8.9% of GDP) than Southeast Asia’s USD 193 billion (6.4% of GDP). Most participating countries show large gains, especially the smaller countries of South Asia. The comprehensive integration scenario involves: (1) The removal of all tariffs associated with South Asian and Southeast Asian trade; (2) a 50% reduction in associated nontariff barriers; and (3) a 15% reduction in trade costs, reflecting improved trade facilitation and investments in infrastructure.

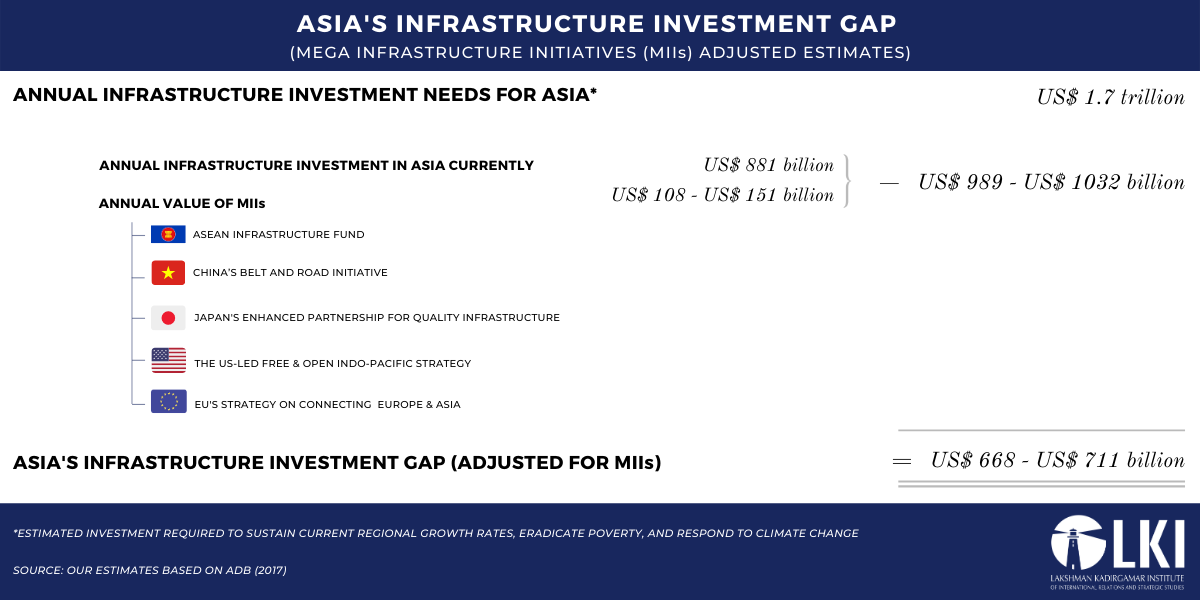

Recent research has examined the plethora of infrastructure challenges, globally, and in Asia. The enormous infrastructure investment gap—the difference between investment needs and current investment levels—has been identified as one of the most pressing issues (Peel and Mitchell, 2017). Studies vary in their methodologies and estimates of infrastructure investment gaps. McKinsey Global Institute (2016) found that the world invests USD 2.5 trillion a year in infrastructure, while USD 3.3 trillion is required annually from 2016 until 2030 to support projected growth. This means that the annual world infrastructure investment gap is USD 0.8 trillion. A particularly glaring infrastructure investment gap is said to exist in Asia. The Asian Development Bank (ADB) (2017) found that Asia annually invests USD 881 billion a year in infrastructure while USD 1.7 trillion a year is needed until 2030 to maintain regional growth, eradicate poverty and respond to climate change.2 The region’s infrastructure investment gap is USD 819 billion per year until 2030.

Asia’s enormous investment gap has encouraged a new form of infrastructure investment, namely the growth of MIIs led by major global economies. MIIs typically operate in a turnkey manner to deliver large scale infrastructure projects to recipients on an international scale. Some MIIs portray vast geographical ambition, covering much of Asia, and beyond. MIIs provide huge amounts of infrastructure financing to recipients as a mix of grants and commercial loans or purely commercial loans. Intermediate inputs, capital goods, and construction services are also imported under tied aid arrangements from major global economies. Limited sourcing of inputs or services from recipients occurs under MIIs.

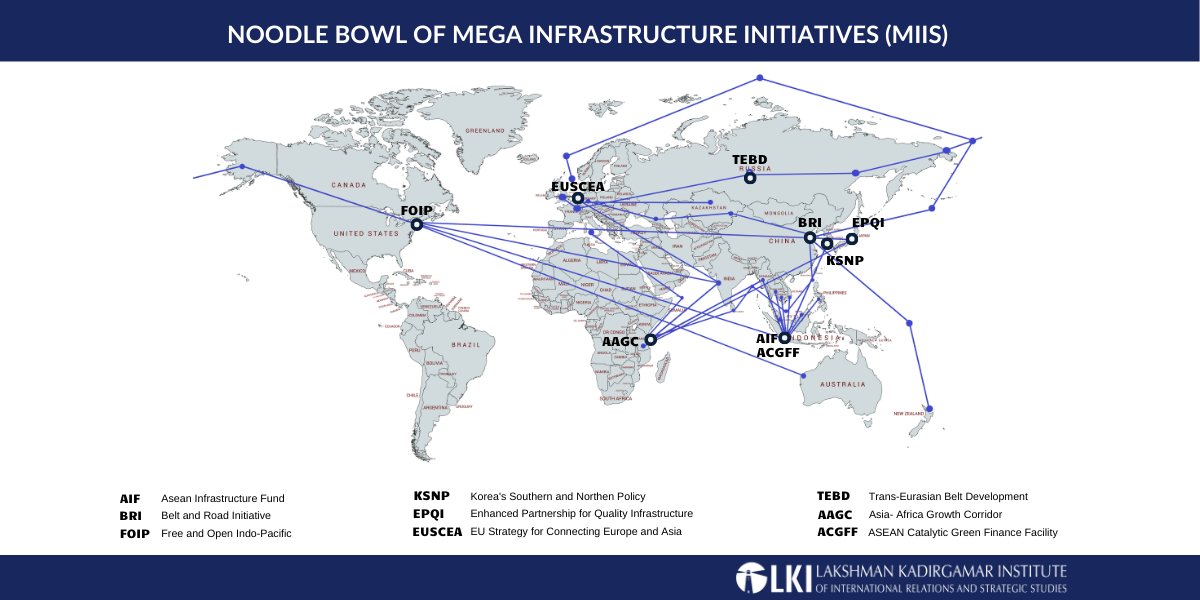

The study of MIIs is challenging because of inadequate data about the operation of MIIs, including project pipelines, financial terms, and procurement procedures. For instance, official information is absent about plans for Korea’s Northern and Southern Policy or Russia’s Trans-Eurasian Belt Development. Information is also scant for three other MIIs known to exist—Russia’s Trans-Eurasian Belt Development of 2015, the Asia-Africa Growth Corridor of 2017 led by India and Japan, and, South Korea’s Northern and Southern Policy of 2017 (Shephard, 2017). But the financial commitments and scope, although not yet determined, may be relatively small for these initiatives. Furthermore, neither China’s Belt and Road (BRI) nor Japan’s Partnership for Quality Infrastructure (PQI)—which have had signature projects under implementation for some time—post online a complete list of projects and the financial terms granted to recipients in Asia. The ASEAN Infrastructure Fund (AIF) seems to be more transparent and provides details of financial terms for its project pipeline as many of its projects are being implemented by multilateral development banks (MDBs).

A comparative analysis of the features of five important MIIs involved in Asia was undertaken by compiling data from different sources in Table 1. The data suggest four observations.

First, having emerged in the decade since the global financial crisis of 2008-2009, MIIs are a recent feature of Asia infrastructure development space. The first movers in 2013 were China’s ambitious BRI and the much smaller ASEAN AIF. These were followed in 2015 by Japan’s significant PQI, and in 2016 its Enhanced Partnership for Quality Infrastructure (EPQI). In 2017, the US-led Free and Open Indo-Pacific Strategy (FOIP) was launched, and in 2018, the EU Strategy for Connecting Europe and Asia.

Second, akin to foreign aid programmes, MIIs appear to be driven by a mix of economic, commercial, and geopolitical motives.3 These range from providing broad philanthropic support to improve connectivity in poorer parts of Asia to narrowly promoting the commercial interests of state-owned enterprises (SOEs) and multinational enterprises (MNCs) of major economies. Export of surplus capital and manpower is a related motive. Security motives also seem to loom large in some MIIs including cyber-security threats, defence-related interests, strategic competition between major powers, and freedom of navigation in critical Asian sea-lanes.

Third, MIIs vary significantly in their geographical ambition and resource envelope. China and Japan’s MIIs seem more ambitious geographically and have committed more funds than the US and EU. In fact, China’s initiative (USD 340 billion) is larger than those of the US (USD 70 billion) and EU (USD 140 billion) combined, if one takes the lower end estimate of the BRI. It is also larger than Japan’s EPQI (USD 200 billion). Meanwhile, ASEAN’s initiative (USD 4 billion) is a fraction of the size of the other four MIIs listed in Table 1.

Fourth, the MIIs listed in Table 1 collectively only make a modest contribution to financing Asia’s enormous infrastructure needs. Figure 1 provides some details of our estimate of their impact. The top line shows the ADB (2017) figure for the region’s annual infrastructure needs of USD 1.7 trillion until 2030. From this is subtracted (1) the annual regional infrastructure spending figure of

USD 881 million from ADB (2017) and (2) our estimate of the combined annual value of the five mega regional infrastructure initiatives which comes to between USS 108 billion to $151 billion.4 The balance amount of USD 668 billion to USD 711 billion annually until 2030 is taken as the region’s revised infrastructure investment gap (MII adjusted estimate). Financing Asia’s unmet infrastructure needs thus remains a significant development challenge for the region’s economies in spite of additional financing from MIIs.

MIIs are much more ambitious and complex than arguably simpler two-country infrastructure projects. At the regional level, MIIs may not solve Asia’s infrastructure investment gap but they do make a useful dent in it. Over time, MIIs may be scaled up and can help further reduce the region’s infrastructure investment gap. At the national level, well designed and implemented MIIs and projects within them, can improve the quality of infrastructure in Asian economies. Nonetheless, some initiatives seem better designed than others; with deep project management, high-quality engineering solutions, strong buy-in from recipients, sizable financial commitments, and support from MDBs with high standards. As good management, engineering, and donor practices spread, laggard initiatives may well emulate their predecessors; a coherent and transparent architecture of MIIs might one day emerge in Asia.

Aside from an information deficit, multiple and overlapping mega infrastructure initiatives in Asia also risk creating a ‘noodle bowl’ phenomenon. The ‘noodle bowl’ effect, which is more typically associated with free trade agreements (FTAs) in Asia, refers to a situation in which a growing number of overlapping arrangements generate increasingly complex rules and standards which give rise to significant transaction costs for economies and business (Kawai and Wignaraja, 2011). A similar analogy can be applied to the more recent spread of mega infrastructure initiatives (Wignaraja, 2015 and 2019). These initiatives share the goal of financing infrastructure in Asia and largely focus on similar sectors. However, they differ significantly in their vision, scale and terms of financing, implementation strategies, procurement approaches, and the actors involved.

The risk of an entangled ‘noodle bowl’ of MIIs in Asia may be exacerbated by three factors.

First, scarce finance may be packaged in a complex way that could make the ‘noodle bowl’ effect more pronounced. As mentioned above, Asia has a large infrastructure investment gap. Recipients and donors want to stretch these limited funds in clusters of projects and individual projects through innovative financial means; such as procurement rules favouring single sourcing by SOEs and MNCs from the donor economy, co-financing mega projects with MDBs, state guarantees to incentivise private investors, fully-fledged public private partnerships (PPPs), and re-packing of various financing instruments. Governments often need to finance increased spending for mega infrastructure

projects in cash-strapped national budgets through international bond issues. Indeed, a bewildering array of partnerships, instruments, and financial terms will likely make managing the financing of infrastructure projects more difficult to fathom by recipients and coordinate among the various actors. The more complex the project and the larger the number of bidders, the more difficulties for recipients.

The potential ‘noodle bowl’ problem is illustrated by a high-speed rail (HSR) project in Indonesia, Southeast Asia’s largest economy. Indonesia wished to build a 150 km HSR link from Jakarta to the country’s fourth largest city, Bandung, and attracted the interest of Chinese and Japanese consortiums during tendering (See Prasad, 2018). This was a new technology to the country, which lacked the capability. The Japanese side undertook careful feasibility studies over five years and thought the deal was clinched in 2015. However, a Chinese bid undercut Japan’s offer and altered the project specifications. Unlike the Japanese offer, the Chinese one did not need a full sovereign guarantee from Indonesia. A bidding race followed with each consortium offering more financing and reducing the implementation timeline. Construction began in 2016 after the Chinese side won the contest but stalled due to mounting project costs and financing problems. It is expected to be completed in 2021 at an escalating cost from the initial quoted figure of about USD 6 billion. The next rail project—to upgrade the railway line between Jakarta and Surabaya—was awarded to Japan, which signalled that Indonesia wanted to maintain a competitive environment for rail tenders. However, it meant that Indonesia now had two vastly different HSR rail systems, which could strain its limited technical and operating capacity. If future HSR projects are awarded to consortiums from other major economies, the ‘noodle bowl’ problem could be exacerbated for Indonesia.

Second, intense selling by some bidders from major economies under MIIs can lead to “white elephant” projects which pose economic risks to participating economies. Lucrative project contracts coupled with a lack of transparency in tendering procedures provide incentives for rent-seeking activity in recipients. A recipient’s infrastructure landscape could become littered with large infrastructure projects which are over-budget, loss-making, and low-return generating. The consequences are debt sustainability, governance, and transparency issues in participating countries. Asian economies, with weaker financial capacity and governance standards, may be more susceptible than richer countries to these risks, and may find that their implementation capacity is overstretched.

The Hambantota Port project in Sri Lanka – a classic small open economy in Asia – illustrates both the issues and a way forward. A decision was taken during the regime of President Mahinda Rajapaksa (2005-2015) to accelerate the development of Hambantota—a economically under-developed region in Southern Sri Lanka with high levels of youth unemployment—through infrastructure investment. A key project was a major transshipment port at Hambantota in the early 2000s, which was expected to become the country’s second largest port after Colombo Port. With financing from the Export Import Bank of China (three fixed interest rate loans totalling US$1.4 billion), China Harbour Engineering Company (CHEC), a Chinese state-owned enterprise (SOE) constructed the port. It seems that comprehensive technical feasibility and market studies were not undertaken for the port project. Taking longer than expected to come on stream, the project incurred financial losses and put a strain on Sri Lanka’s public finances. A chequered history has led some to portray Hambantota Port as a case study of unprofitable infrastructure investment and China’s “debt trap diplomacy”.5 It has been characterised a strategic asset seizure whereby China forcibly took control over Hambantota Port when the Sri Lankan government was allegedly unable to repay the loans that financed port construction.

However, this portrayal seems a one-sided and dated narrative of the Hambantota Port Project. A debt for equity swap implies that loans to China are forgiven or refinanced in exchange for equity. This is not what happened. To stem the financial losses, in 2017 the coalition government of President Sirisena agreed to give China a controlling interest in managing the port on a 99-lease. Under the risk sharing agreement, Sri Lanka received a sum of USD 1.12 billion which was used to bolster the country’s foreign exchange reserves and retained ownership of the port. Furthermore, the management of the Hambantota Port moved to one of China’s best run SOEs, China Merchant Port Holdings Company Limited. This global port operator is not only developing Hambantota Port and the adjacent industrial zone but also working to diversify the range of port related services (e.g. ship repairing, and bonded warehousing and distribution). Once Hambantota Port becomes fully operational over the next few years, container traffic through Sri Lanka may double to some 16 million TEUs. The industrial zone is expected to attract foreign investment and create jobs.

Finally, although Sri Lanka may face a general foreign debt problem, this has little to do with Chinese loans (see Wignaraja, et al., 2020). Nonetheless, to guard against the risk of a Chinese debt trap in the future, Sri Lanka should strengthen the debt management system to reduce vulnerabilities and to improve debt transparency with international assistance. It should also request a short-term debt service suspension on Chinese debt to facilitate overall debt sustainability and increase its share of infrastructure financing from the AIIB, which offers low-cost infrastructure finance at high procurement and environmental standards.

The problem of ‘white elephant’ projects seems better illustrated by the Sinamale bridge project6 in the Maldives, a strategically located group of dispersed atolls in the Indian Ocean. The Maldives wanted to build its first inter-island sea bridge, 2.1 km long, between the airport and the wider metropolitan island of Hulumale and the capital city, Male (Saara, 2019). An Indian and a Chinese company bid for the project, which the latter won. The bridge opened in 2018. The original project cost of USD 210 million—which allegedly over-ran to USD 300 million—was financed by a part grant and part commercial loan from China under the BRI initiative during the administration of

former President Yameen Abdul Gayoom. Cost-recovery was limited due to nominal toll fees for vehicles. The project is also clouded by allegations of corruption and debt trap diplomacy (Macan-Markar, 2019). The incoming administration of President Ibrahim Mohamed Solih allege that the Maldives paid for a four-lane vehicular bridge but only got two lanes. An investigation is planned into BRI projects in the Maldives.

Third, MIIs will likely create winners and losers. Winners arise when initiatives (i) reinforce comparative advantage reflected in trade and foreign direct investment (FDI) patterns in Asia, to avoid the risk of “building ports and airports to nowhere;” (ii) are backed by open regionalism initiatives and domestic structural reforms; (iii) incorporate adequate safeguards (e.g., for the environment and resettlement) in formulating projects; and (iv) coordinate among themselves in key areas such as planning, project formulation, procurement practices, financing, and implementation.

Losers from initiatives are hard to predict, as the devil is in the detail for specific projects. Landlocked countries like Nepal, or island states like the Maldives or Fiji, that are somewhat excluded from MIIs may be marginalised. The same might apply to distant provinces within large Asian economies like Indonesia or Bangladesh. Some transport routes—either land or maritime transport, for instance—and some workers, such as port workers, may also fail to benefit from efficiency-seeking PPPs.

Ironically, the quest to maximise the benefits of MIIs could contribute to the “noodle bowl.” Asian economies should collectively adopt offsetting measures in order to avoid this outcome and mitigate the negative effects of such initiatives. Creating Asian variants of the EU’s regional development funds would address regional development imbalance; these funds are best established under the framework of sub-regional cooperation bodies like ASEAN, Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC), or Indian Ocean Rim Association (IORA).

As more MIIs are established, the likelihood of Asian “noodle bowl” risks increase, as does the transactions costs for economies and business. Several actions are needed to mitigate these risks and costs in Asian recipients including small economies.

First, Asian recipients need to do their homework to efficiently utilise the package of finance and expertise from MIIs to raise national economic development. This means the following measures:

Second, in view of the long gestation period of infrastructure projects and the potential risk of white elephant projects under MIIs, holding a national dialogue on infrastructure development can help to reduce economic risks. The draft national infrastructure master plan should be the basis for such a dialogue, which should be attended by all political parties, ministries of finance and central bank officials, academics, business, civil society, and the media. Successful small Asian economies have managed the difficult exercise of forging a national consensus on infrastructure development in a transparent manner.

Third, embedding the financing requirements for infrastructure projects in economic reform programmes—either home-grown or under the preview of the Internal Monetary Fund (IMF) and the World Bank—is a necessary task for implementing a stable and predictable macroeconomic policy.

Fourth, major powers should attempt to implement more borrower ownership of projects under MIIs. This means being more transparent and releasing project-level data (including agreements with governments, financial terms, and feasibility studies), providing comprehensive training for national counterparts, and adhering to strict anti-corruption standards in projects. Where possible, local sourcing of raw materials, sub-contracting to local firms and promoting localisation of project management would also be a useful step in promoting borrower ownership.

Fifth, Asian recipients should help to operationalize middle-power agency and regional cooperation. Small Asian economies should look to regional forum such as ASEAN, SAARC, BIMSTEC, and IORA to engage in constructive policy dialogues on infrastructure finance with middle powers. Furthermore, to advance middlepower agency, middle powers themselves need to become more proactive in developing alternative approaches to providing public goods like infrastructure finance (See Stromseth, 2020).

This LKI Policy Brief explored the crowded field of MIIs in Asia in order to assess their economic impact and ways which Asian recipients might navigate them in a COVID era of negative or slow world growth. It focused on the growth of China’s BRI, Japan’s PQI, the ASEAN AIF, the US-led FOIP, and Europe’s EUSCEA.

A review of literature and development experience highlighted the link between infrastructure investment and economic development in Asia. A large infrastructure investment gap exists which has encouraged the growth of MIIs led by major global economies. Data gaps and limited transparency have made it difficult to study the effects of MIIs. Mapping data from various sources offers interesting insights on the features of major MIIs. While these initiatives are of recent origin they differ significantly in their motivations, ambition, financial commitments, and sectoral coverage.

Several implications can be drawn from the analysis for Asian recipients grappling with the effects of COVID. First, major global economies deserve credit for trying to solve Asia’s large infrastructure investment gap with MIIs and various project pipelines. However, the growth of such initiatives may give rise to an Asian “noodle bowl” of multiple overlapping initiatives, which could raise transactions costs for small regional economies. Second, it is important for small Asian economies to develop coherent national strategies to reap the benefits while minimising the costs of MIIs. Developing a medium-term national infrastructure master plan and ensuring prudent macroeconomic and debt management are important elements of national strategy. Third, major economies can support borrower ownership of projects in Asian recipients through technical assistance for things like improved data collection, and capacity building and training in infrastructure development and anti-corruption measures.

These are the early days for MIIs in Asia and the story of how they might affect recipients in the COVID era is still unfolding. Clearly, more thought and time are needed to ensure that these initiatives are in tune with the ambition of Asian recipients to transit to upper middle-income and high-income status in a fragile world economy hamstrung by COVID.

1This Policy Brief builds on Wignaraja (2015 and 2019).

2In ADB (2017), Asia’s needs for 45 developing market economies from 2016-2030. This includes the costs of climate mitigation and adaptation. The region’s investment is for 25 economies with adequate data.

3Speeches by President Xi Jinping (2017) on the BRI, Secretary Mike Pompeo (2018) on the FOIP and Prime Minister Abe on the EPQI (METI, 2016) provide insights on the MIIs strategies of major global economies.

4Our estimate (assuming a BRI lower bound estimate of US$340 billion) of the combined value of the five initiatives in Table 1 gives a figure of about $754 billion over a 5-7 year time horizon. This works out to between US$108 to $151 billion annually. Assuming that the financing in mega infrastructure initiatives is additional money and only spent in Asia, the region’s infrastructure investment gap only reduces to between US$668 to US$711 billion annually until 2030.

5Chellaney (2017) was an early proponent of Sri Lanka falling into a Chinese debt trap. Thorne and Spevack (2017) explore the link between China’s investment in the Hambantota Port and geopolitical strategy. They argue that the terms of 99-year lease on Hambantota Port favour China, that the investment generated political influence and that Chinese debt constricts Sri Lankan policy. This narrative has been challenged by Wignaraja et.al. (2020).

6Also referred to as the China-Maldives Friendship Bridge.

ADB. (2017), Meeting Asia’s Infrastructure Needs, Manila: Asian Development Bank.

Arnold, J. (2009), “The Role of Transport Infrastructure, Logistics and Trade Faciliation in Asia’s Trade”, in Francois, J., Rana, B.P., & Wignaraja, G. (eds), Pan-Asian Integration: Linking East and South Asia. Basingtoke (UK): Palgrave Macmillan.

Chellaney, B. (2017), “China’s Creditor Imperialism”. Project Syndicate, [Online] Available at: https://www.project-syndicate.org/commentary/china-sri-lanka-hambantota-port-debt-by-brahma-chellaney-2017-12?barrier=accesspaylog [Accessed 01 August 2020].

Macaes, B. (2019), Belt and Road: A Chinese World Order, Gurgaon: Penguin Random House India.

Hillman, J. (2018), “How Big is China’s Belt and Road?”, CSIS Commentary, 3 April 2018.

Islam, A., Salim, R., & Bloch, H. (2016), “Does Regional Integration Affect Efficiency and Productivity Growth? Empirical Evidence from South Asia”, Review of Urban and Regional Development Studies, 28(2): pp. 107-122.

Izumi, H. (2017), “Quality Infrastructure Investment: Global Standards and New Finance”, Presentation by Special Advisor to the Prime Minister of Japan at the First International Economic Forum on Asia, 14 April 2017, Tokyo, Japan.

Jinping, Xi. (2017), “Work Together to Build the Silk Road Economic Belt and The 21st Century Maritime Silk Road”, [Online] Xinhuanet.com. Available at: http://news.xinhuanet.com/english/2017-05/14/c_136282982.htm [Accessed 21 July 2020].

Kawai, M., & Wignaraja, G. (eds). (2011), Asia’s Free Trade Agreements: How is Business Responding? Cheltenham, UK: Edward Elgar.

Krugman, P. (1991), Geography and Trade. Cambridge (Mass): MIT Press.

Kumagai, S., Hayakawa, K., Isono, I., Keola, S., & Tsubota, K. (2013), “Geographical Simulation Analysis for Logistics Enhancement in Asia”, Economic Modelling 34(C): pp.145–153.

Kynge, J. (2016), “How the Silk Road plans will be financed”, [Online] The Financial Times. Available at: https://www.ft.com/content/e83ced94-0bd8-11e6-9456-444ab5211a2f?mhq5j=7 [Accessed 01 August 2020].

Macan-Markar, M. (2019), “Maldives Election Paves Way for China Deal Investigation”, [Online] Nikkei Asian Review. Available at: https://asia.nikkei.com/Spotlight/Belt-and-Road/Maldives-election-paves-way-for-China-deals-investigations [Accessed 20 July 2020].

McKinsey Global Institute. (2016), Bridging Global Infrastructure Gaps, [Online] Available at: https://www.mckinsey.com/industries/capital-projects-and-infrastructure/our-insights/bridging-global-infrastructure-gaps [Accessed 31 July 2020].

METI. (2016), “G7 Ise-Shima Summit “Expanded Partnership for Quality Infrastructure”, Ministry of Economy, Trade and Industry (METI), Japan, [Online] Available at: https://www.meti.go.jp/english/press/2016/0523_01.html [Accessed 01 August 2020].

Peel, M., & Mitchell, T. (2017), “Asia’s $26tn infrastructure gap threatens growth, ADB warns”, [Online] The Financial Times. Available at: https://www.ft.com/content/79d9e36e-fd0b-11e6-8d8e-a5e3738f9ae4?mhq5j=e7 [Accessed 01 August 2020].

Poling, G.B. (2020), “America First versus Wolf Warriors: Pandemic Diplomacy in Southeast Asia”, CSIS Commentary, 18 June.

Pompeo, M. (2018). “America’s Indo-Pacific Economic Vision” Keynote Address at the Inaugural Indo-Pacific Business Forum, US Chamber of Commerce, 30 July, Washington DC, [Online] Available at: https://asean.usmission.gov/sec-pompeo-remarks-on-americas-indo-pacific-economic-vision/ [Accessed 01 August 2020].

Prasad, R. (2018), “The China-Japan Infrastructure Nexus: Competition or Collaboration”, The Diplomat, 18 May.

Saara, F. (2019), “My Story: Bridge of Hope for the Maldives”, [Online] CGTN Website. Available at: https://news.cgtn.com/news/3d3d414d7959444d34457a6333566d54/index.html [Accessed 01 August 2020].

Shepard, W. (2017), “India And Japan Join Forces To Counter China And Build Their Own New Silk Road”, [Online] Forbes. Available at: https://www.forbes.com/sites/wadeshepard/2017/07/31/india-and-japan-join-forces-to-counter-china-and-build-their-own-new-silk-road/#621838f44982 [Accessed 19 July 2020].

Stiglitz, J.E. (2001), “From Miracle to Crisis to Recovery: Lessons from Four Decades of East Asian Experience” in J.E Stiglitz and S. Yusuf (eds.), Rethinking the East Asian Miracle. Oxford: Oxford University Press.

Stromseth, J. (2020), Beyond Binary Choices: Navigating great power competition in Southeast Asia. Foreign Policy at Brookings: Washington DC, [Online] Available at: https://www.brookings.edu/wp-content/uploads/2020/04/Beyond-Binary-Choices-Jonathan-Stromseth-April-2020.pdf [Accessed 19 July 2020].

Thorne, D., & Spevack, B. (2017), Harbored Ambitions: How China’s Port Investments Are Strategically Reshaping the Indo-Pacific, A Report by C4ADS: Washington DC, [Online] Available at: https://static1.squarespace.com/static/566ef8b4d8af107232d5358a/t/5ad5e20ef950b777a94b55c3/1523966489456/Harbored+Ambitions.pdf [Accessed 19 July 2020].

Venables, A.J. (2019), “Economic Geography and Trade”, Oxford Research Encyclopaedias: International Economics. Online publication. February 2019. DOI: 10.1093/acrefore/9780190625979.013.332

Wignaraja, G. (2015), “Mega-Regional Infrastructure Initiatives – Asia’s New Noodle Bowl? Asian Development Blog, [Online] Available at:https://blogs.adb.org/blog/mega-regional-infrastructure-initiatives-asia-s-new-noodle-bowl [Accessed 19 July 2020].

Wignaraja, G. (2019), “Assessing the Costs and Benefits of Mega Infrastructure Initiatives in Asia”, in Panorama Insights on Asian and European Affairs, 14 August 2019, Singapore: Konrad Adenauer Stiftung Regional Programme on Political Dialogue in Asia, [Online] Available at: https://www.kas.de/web/politikdialog-asien/single-title/-/content/trade-and-economic-connectivity-in-the-age-of-uncertainty [Accessed 19 July 2020].

Wignaraja, G., Morgan, P., Plummer, M., & Zhai. F. (2015), “Economic Implications of Deeper South Asian-Southeast Asian Integration: A CGE Approach”, Asian Economic Papers, 14(3): 63-81.

Wignaraja, G., Panditaratne, D., Kannangara, P., & Hundlani, D. (2020), “Chinese Investment and the BRI in Sri Lanka, Research Paper, London: Chatham House, [Online] Available at: https://www.chathamhouse.org/publication/chinese-investment-and-bri-sri-lanka [Accessed 20 April 2020].

*Ganeshan Wignaraja is the Executive Director at the Lakshman Kadirgamar Institute of International Relations and Strategic Studies (LKI) in Colombo. The opinions expressed in this piece are the author’s own and not the institutional views of LKI, and do not necessarily reflect the position of any other institution or individual with which the author is affiliated.

24 Horton Place

Colombo 7

Sri Lanka

A think tank engaging in independent research of Sri Lanka’s international relations and strategic interests, to provide insights and recommendations that advance justice, peace, prosperity, and sustainability.