November 24, 2017 Reading Time: 12 minutes

Reading Time: 12 min read

Image credit: narendramodiofficial / flickr

The rise of Asia’s giants provides fascinating insights on the unpredictable nature of economic development. China grew much faster than India over several decades and is challenging the global dominance of industrial countries. Favourable initial conditions, a first mover advantage and gradual economic reforms with a strong state role helps to explain the difference in the growth record of China and India. A demographic dividend and a recent pickup in Indian reforms has yielded improved growth. Meanwhile, with rising wages, China’s growth has slowed leading it to launch the ambitious Belt and Road (BRI) Initiative. A soft landing, with Chinese growth progressively converging to that of industrial countries, seems the likely scenario. Continuing with reforms and private sector development in both giants can also help sustain their growth.

Dr. Ganeshan Wignaraja*

The remarkable growth of China and India has shifted the centre of the world economy towards Asia. However, the 2008 global financial crisis exposed vulnerabilities in the export-led model of Asia’s two economic giants. Meanwhile, guided by President Trump’s “America First” nationalism, the United States is appearing more isolationist on the world stage. With the IMF predicting a recovering world economy in 2018 amid policy uncertainty, the economic strategies of the giants are under the microscope. The slowdown in China’s growth and risks to India’s outlook have fuelled debate on whether their respective strategies can sustain regional and global growth. This policy brief charts the rise of the giants, evaluates the role of reforms on their performance and discusses their medium-term economic outlook.

Figure 1

Source: IMF, World Economic Outlook Database, Accessed October 2017

China and India have followed similarly impressive growth trajectories in recent decades but the emergence of China is regarded as one of biggest growth surprises of the twentieth century.1

While China began to open its economy to market forces and foreign direct investment (FDI) in 1978 – more than a decade before India – both countries have enjoyed years of rapid growth that has lifted millions out of poverty. China grew at a historically unprecedented 10% per year during 1980-2006 and India at a respectable 6% (see Figure 1). Together the giants took an astonishing 806 million people out of poverty (measured as the % of population living on less than $1.90 per day) between 1993 and 2013. The two Asian giants’ exports increasingly comprise sophisticated manufactures and services, rather than simple labour-intensive products.

Moreover, after years of tepid growth after the global financial crisis, 2018 seems bright. The latest IMF forecasts suggest that rapid growth is expected in both countries in 2018 – over 6.5% in China and 7.4% in India.2 This is partly linked to a recovery in demand in advanced economies, which are expected to grow at 2% in 2018. The United States is in recovery mode and the outlook of the EU and Japan is more positive than before. As a result, the world economy is expected to grow at 3.7% in 2018.

In achieving its pre-eminent status, China benefitted from favourable initial conditions including a large domestic market, low-cost productive labour, and the geographical advantage of its proximity to Japan – the previous engine of Asian growth. China also benefitted from a coherent policy vision articulated by an 80 million strong Chinese Communist Party. Even more importantly, China pursued gradual and coordinated economic reforms, beginning in 1978, which served as a catalyst for subsequent decades of growth. Titled “Market Socialism with Chinese Characteristics”, by Deng Xiaoping, the reform programme emphasised a strong role for the state alongside controlled opening to market forces.3

Opening the door to FDI was at the heart of ushering in market forces. Key steps included (i) a law to encourage joint ventures between foreign and local investors, (ii) establishment of special economic zones (SEZs) with tax incentives for FDI on the Southern coast, (iii) steady liberalisation of a controlled import regime and (iv) a duty drawback scheme to ensure duty-free access for all imported inputs for export processing. The 1978 reforms also marked the beginning of the revival of local private business in China, which had long been stigmatised as the root of evil behaviour.

China’s accession to the World Trade Organization (WTO) in 2001 was another important step in its process of global integration. This move brought with it tariff cuts, services sector liberalisation with FDI allowed and an improved intellectual property protection regime.

The state continued to play a role in economic activity. Central planning has remained a feature of macroeconomic and sectoral resource allocation. China has a straggling array of state-owned enterprises (SOEs) with millions of employees across all sectors of the economy. More controversially, following in the footsteps of Japan and Korea, China used various industrial policy instruments (finance, subsidies, local content rules) to foster globally competitive large firms. However, China’s record on industrial policy is mixed. Notable recent successes such as high-speed trains, the Comac C-919 commercial jet and defence activities (e.g. a home grown aircraft carrier) sit alongside some failures (e.g. China’s home-grown 3G mobile-technology).

India did attempt some partial and half-hearted economic liberalisation measures during 1976-1991. However, 4 serious economic liberalisation in India did not begin until 1991 – more than a decade later than China – and it focused more narrowly on easing restrictions on FDI and imports. They also increased the investment limit of small and medium enterprises (SMEs) and permitted free determination of interest rates by banks. The private sector was seen as the new engine for growth with the state playing a distinct role. Furthermore, the focus of economic policy making in India shifted to the Ministry of Finance and the previously mighty Planning Commission assumed a subsidiary role. These reforms, termed “the New Economic Policy” or NEP, were initiated by the government of Prime Minister Narashima Rao.5

In recent years India has accelerated reform of FDI entry regulations and import tariffs. For instance, India’s simple average import tariffs for manufactures reached 7.8% for manufactures in 2015 compared with 6.4% for China. Nonetheless, as a result of China’s “first-mover” advantage, more credible implementation and a more comprehensive reform programme, it has been able to achieve consistently higher growth than India for the past several decades and has a much larger share of world GDP than India.

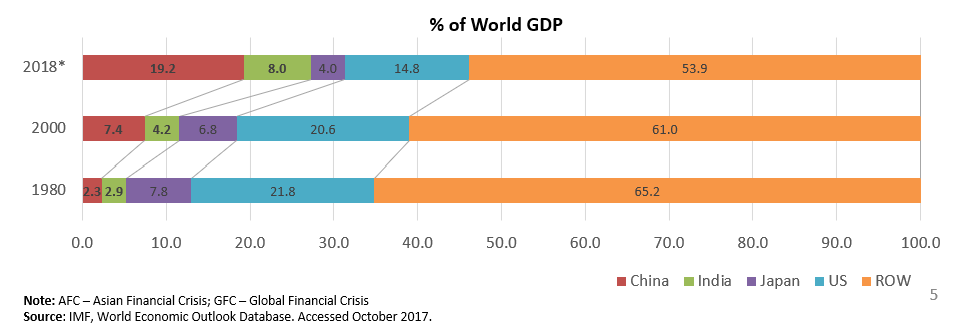

Figure 2

Source: IMF, World Economic Outlook Database, Accessed October 2017

From 2.3% of world GDP in 1980, China will increase its share to 19.3% in 2018 (see Figure 2). Although the initial base was the same, India’s increase in world GDP has been somewhat more modest from 2.9% to 8%. Over the same period, the US share declined from 21.8% to 14.8%, while that of Japan dropped from 7.8% to 4%. Thus, the giants appear to be increasingly replacing advanced economies as drivers of world growth. This has led some to talk about a multi-polar global economy as underpinning the future of global growth.

Amid this global rise, China has moved away from a heavy reliance on exports that are resource-based (e.g. food) and low-technology (e.g. textiles, garments and footwear) exports to become the global factory. It is increasingly prominent as the assembly hub of sophisticated global supply chain trade in technology intensive manufactures (e.g. electronic and electrical products, aircraft, precision instruments and pharmaceuticals). For example, while the Apple iPhone was developed in the US, its various components from over 200 industrial suppliers around the world are assembled in a factory in Shenzen that is owned by a firm based in Taiwan. Apple coordinates and sets quality standards for its geographically dispersed suppliers. In 2009-2013, China accounted for 25% of global supply chain trade, up from under 13% in 2001-2014. This compares with 28% for the EU, 8% for Japan and 7% for the US in 2009-2013.6

India’s global supply chain exports have also risen from a tiny base to about 1% in 2009-2013. On the other hand, Indian exports are increasingly led by more-sophisticated, skill-intensive services such as information technology (IT), business process outsourcing (BPO) and financial services. In 2016 India accounted for an impressive 11.2% of world IT exports compared with 5.2% for China. India’s success in the IT trade is explained by widespread use of English, supplies of high-quality graduates from Indian Institutes of Technology and Indian Institutes of Management, falling communications costs and returning non-resident Indian investors from Silicon Valley.7

Both giants have pursued distinctive reforms and have become more outward-oriented than before. Commonly, China and India followed a gradual approach to reforms with improved growth, transformation and poverty reduction. This is in stark contrast to the “Big Bang” reforms in the Soviet Union which resulted in lacklustre economic growth and grim social impacts for millions of people.

In spite of a strong state role, Firms operating in China today generally enjoy a more competitive business environment than their counterparts in India, with more market-friendly rules for business start-ups, property registration, contract enforcement and bankruptcy. For instance, in 2017 China is ranked 78 on the World Bank’s Ease of Doing Business Index compared with 130 for India. Beginning in 1980s, China attracted FDI into manufacturing to serve as the cornerstone of export-led growth. Annual average FDI inflows to China increased nine-fold from $19 billion to a record $159 billion between 1980-1999 and 2000-2016. Technology transfer accompanied FDI inflows while controlled liberalisation of protected industries led to increased efficiency and industrial restructuring.

China’s outward FDI into Asia and beyond has increased substantially in recent years. FDI outflows from China averaged $56 billion per year during 2000-2016.8 It went mainly to neighbouring Asian economies (e.g. Southeast Asian economies and India), the EU and the US. Chinese outward FDI has been driven by easing of regulations on outward investment, internationalisation of Chinese firms to improve productivity, lower labour costs in manufacturing overseas and huge reserves seeking high-yielding assets overseas.

India was slower to adopt comprehensive reforms and in its first decade of reform, which began in 1991, focused more narrowly on easing restrictions on foreign ownership. India also appeared to be less coordinated than China in implementing reforms with a consequent loss of investor credibility. With the recent acceleration of reforms, annual average FDI inflows into India increased from $2 billion to $23 billion between 1980-1999 and 2000-2016. Interestingly, annual FDI flows in India during its second decade of reform compares favourably with those during China’s first reform decade. This illustrates the contrasting effectiveness of reform in the two giants.

Meanwhile, the managed floating exchange rate policies of the two giants have been broadly similar as they both faced tariff reform gradually, seeking to use the exchange rate as a critical tool for encouraging exports.9 Both had success in the 2000s in maintaining favourable real effective exchange rates for exports, although China’s stance provided better incentives for exporters. Both economies particularly China fostered a controlled financial system and kept real interest rates for business lending is somewhat low. Furthermore, state banks were important in directing credit to the private sector and controls in capital flows were a distinct feature.

Both giants have strong leaders with ambitious economic visions. Xi Jinping became China’s President in 2012 and has implemented “change maker” policies. These include ending the One Child Policy to counter an aging population, launching an anti-corruption drive to root out corrupt officials and making the RMB a world reserve currency as a notable step towards the RMB becoming a global currency.

Xi’s signature international initiative is the BRI which some suggest is on a similar scale to the Marshall Plan launched by the US to rebuild Europe after World War Two. The BRI was partly to remedy excess capacity in China and to boost global infrastructure connectivity and growth. It is an ambitious web of intercontinental road, rail and port links involving 60 countries across Asia, Europe and Africa. It is backed by a huge Chinese pledge of least $269 billion7 and project co-financing from international sources like multilateral development banks.

Meanwhile, Indian Prime Minister Narendra Modi assumed office in 2014 and has pursued a radical reform agenda over the last few years. He has implemented a flurry of measures including a nationwide sales tax, a “Make in India” initiative, demonetised large currency notes, introduced fiscal reform and accountability, fostered investment climate reform and created new social security programmes. As a countermove to the BRI, Modi also introduced an “Act East Policy”, to link with high-performing economies in East Asia, and the Africa-Asia Growth Corridor (in collaboration with Japan), to establish a partnership with Africa on infrastructure and skills upgrading.

The recent Xi and Modi reforms mean that both giants have laid the foundation for continued growth. The IMF expects China to grow at 6.3% per year in 2018-2020 and India to grow at a faster rate of 7.7% (see Figure 1). However, it is possible that demonetisation squeezed income of the cash dependent poor and informal sector. Thus, India’s growth may come in below the IMF forecast. Growth in both countries will be driven by not just exports but also heightened domestic and Asian demand. Services – fuelled by growing middle-class consumption – will play an increasingly important part in economic activity in the giants. India’s reforms have made great strides and have begun to catch up with China. India has also boosted public investment in infrastructure and other areas.10 Some of India’s states – Andhra Pradesh, Maharashtra and Tamil Nadu – are becoming manufacturing hubs and linking into global supply chains. Yet China’s economic policies, investment climate and supply-side conditions remain more favourable than India’s. Accordingly, China will continue to lead India in global supply chain trade for the foreseeable future.

India appears to be enjoying a demographic dividend for growth based on an increasingly youthful population.11 Between 2000 and 2015, India added about 20 million youth (i.e. population under 24 years of age) whereas China’s youth population dropped by 80 million. India’s increase in youth is perhaps a mixed blessing. On the positive side, it means that more dynamic young people are entering the labour force. However, India’s tertiary enrolment rate is 27% in 2015 compared with a rate of 43% in China. Furthermore, in 2016 China had 4.7 million STEM (science, technology, engineering and mathematics) graduates while India had 2.6 million. This suggests that India may face a shortage of high-skilled workers, just as the knowledge sector of its economy is poised for continued rapid expansion.

Moreover, China allocates significantly more resources than India to R&D and infrastructure, both key determinants of future growth. China spends as much as 2.1% of GDP on R&D while India spends 0.6%. China’s increasingly pro-active R&D strategy is focusing on the high technology industries of the future such artificial intelligence, robotics, biotechnology and aerospace. Its intent is to become a technological innovator and an Asian technological hub, rather than an imitator of imported technologies from industrial countries. Likewise, China invested 8.6% of its GDP per year during 1992-2013 on infrastructure compared with 4.9% in India.12 In terms of infrastructure quality, China and India are similar in terms of ports, but India lags behind China in railways and electricity supply.

The story of the rise of giants provides fascinating insights on the unpredictable nature of economic development. China grew much faster than India over several decades and is challenging the global dominance of industrial countries. Favourable initial conditions, a first mover advantage and gradual economic reforms with a strong state role helps to explain the difference in the growth record of China and India. A demographic dividend and a recent pickup in Indian reforms has yielded improved growth. Meanwhile, with rising wages and a looming middle income trap, China’s growth has slowed. A soft landing, with Chinese growth progressively converging to that of industrial countries, seems the likely scenario.

The IMF projects that China and India will switch places in terms of future growth in the short term. However, many risks lie ahead which could tilt the giants’ short-term outlook to the downside. These include political uncertainty, trade protectionism, tighter global financial conditions and weak productivity growth, to name a few. India’s growth outlook could be dampened by the transitory effects of demonetisation, the implementation of the nationwide sales tax and subdued private sector investment. China’s outlook is susceptible to systemic risks of a debt bubble in an overly state-controlled financial system, a trade war with the US and a risk of a nuclear confrontation in the Korean Peninsula. How each giant weathers these risks will ultimately determine their economic performance during the next few years.13

A part of China’s policy bet lies in using the BRI to neatly transit to a position of global leadership alongside, or to replace, the increasingly isolationist US. Another is reforming its centrally administered SOEs through mergers, restructuring, cutting capacity and closing “zombie companies”. In contrast, India’s bet seems to be the pursuit of radical domestic reforms and trying to tap into East Asia’s dynamism through various initiatives. In addition, India has scope for emulating China in global supply chains by enhancing supply-side measures, such as boosting literacy and skill creation, and fostering industrial R&D and investing in infrastructure. Continuing with reforms and private sector development in both giants can also help sustain their growth.

1 Winters, L. and Yusuf, S. (2007). Dancing with Giants: China, India and the Global Economy, Washington, D.C.: World Bank.

2 International Monetary Fund (2017). Seeking Sustainable Growth Short-Term Recovery, Long-Term Challenges. World Economic Outlook. [online] Washington, DC. Available at: https://www.imf.org/en/Publications/WEO/Issues/2017/09/19/world-economic-outlook-october-2017

3 Wignaraja, G. (2011). “Economic Reforms, Regionalism and Exports: Comparing China and India”, East-West Center, Policy Studies No. 60. Available at: http://www.eastwestcenter.org/publications/publications-home

4Lin, Justin Yifu (2013). “Demystifying the Chinese Economy, “The Australian Economic Review, Vol46:3, P 259-268.

5Bhagwati, J. and Panagariya, A. (2014 edited). Reforms and Economic Transformation in India, Oxford: Oxford University Press.

6 Wignaraja, G. (2016 edited). Production Networks and Enterprises in East Asia: Industry and Firm-level Analysis, Heidelberg: Springer.

7 Wignaraja, G. (2012). “Commercial Policy and Experience in the Giants: China and India” in M. E. Kreinin and M.G. Plummer (ed.), The Oxford Handbook of International Commercial Policy, Oxford: Oxford University Press.

8 World Bank (2017), World Development Indicators Database. Available at: https://data.worldbank.org/data-catalog/world-development-indicators

9 Goldstein, M. and Lardy, N. (2006). China’s Exchange Rate Policy Dilemma. American Economic Review, 96(2), pp.422-426.

10McKinsey Global Institute (2016). Bridging Global Infrastructure Gaps. [online] Available at: https://www.mckinsey.com/industries/capital-projects-and-infrastructure/our-insights/bridging-global-infrastructure-gaps

11Aiyar, S. and Mody, A. (2013), “The Demographic Dividend: Evidence from the Indian States” in S. Shah, B. Bosworth and A. Panagariya (eds), India Policy Forum 2012/2013, New Delhi: Sage Publications.

12 McKinsey Global Institute (2016). Bridging Global Infrastructure Gaps. [online] Available at: https://www.mckinsey.com/industries/capital-projects-and-infrastructure/our-insights/bridging-global-infrastructure-gaps

13 ADB and ADBI (2014). ASEAN, PRC and India: The Great Transformation. Manila and Tokyo: Asian Development Bank and ADB Institute. Available at: http://www.adbi.org/files/2014.09.16.book.asean.prc.india.transformation.pdf

Jinping, Xi (2017). Full text of President Xi’s speech at opening of Belt and Road forum – Xinhua | English.news.cn. [online] Available at: http://news.xinhuanet.com/english/2017-05/14/c_136282982.htm

Modi, Narendra (2017). Read the Full Transcript of Indian Prime Minister Narendra Modi’s Independence Day Speech. [online] Available at: http://time.com/4901564/narendra-modi-india-70-independence-day-speech/

*Dr. Ganeshan Wignaraja is the Chair of the Global Economy Programme at the Lakshman Kadirgamar Institute of International Relations and Strategic Studies (LKI) in Colombo. The author acknowledges the assistance of Dr. Dinusha Panditaratne and Pabasara Kannangara. This policy brief is a revised version of the inaugural lecture delivered at the Lakshman Kadirgamar Institute of International Relations and Strategic Studies (LKI) on the 31 October 2017. All errors and omissions remain the author’s. The opinions expressed in this article are the author’s own and not the institutional views of LKI. They do not necessarily represent or reflect the position of any other institution or individual with which the author is affiliated.

24 Horton Place

Colombo 7

Sri Lanka

A think tank engaging in independent research of Sri Lanka’s international relations and strategic interests, to provide insights and recommendations that advance justice, peace, prosperity, and sustainability.